Workspace

Preview · in developmentThe Analyst Workspace

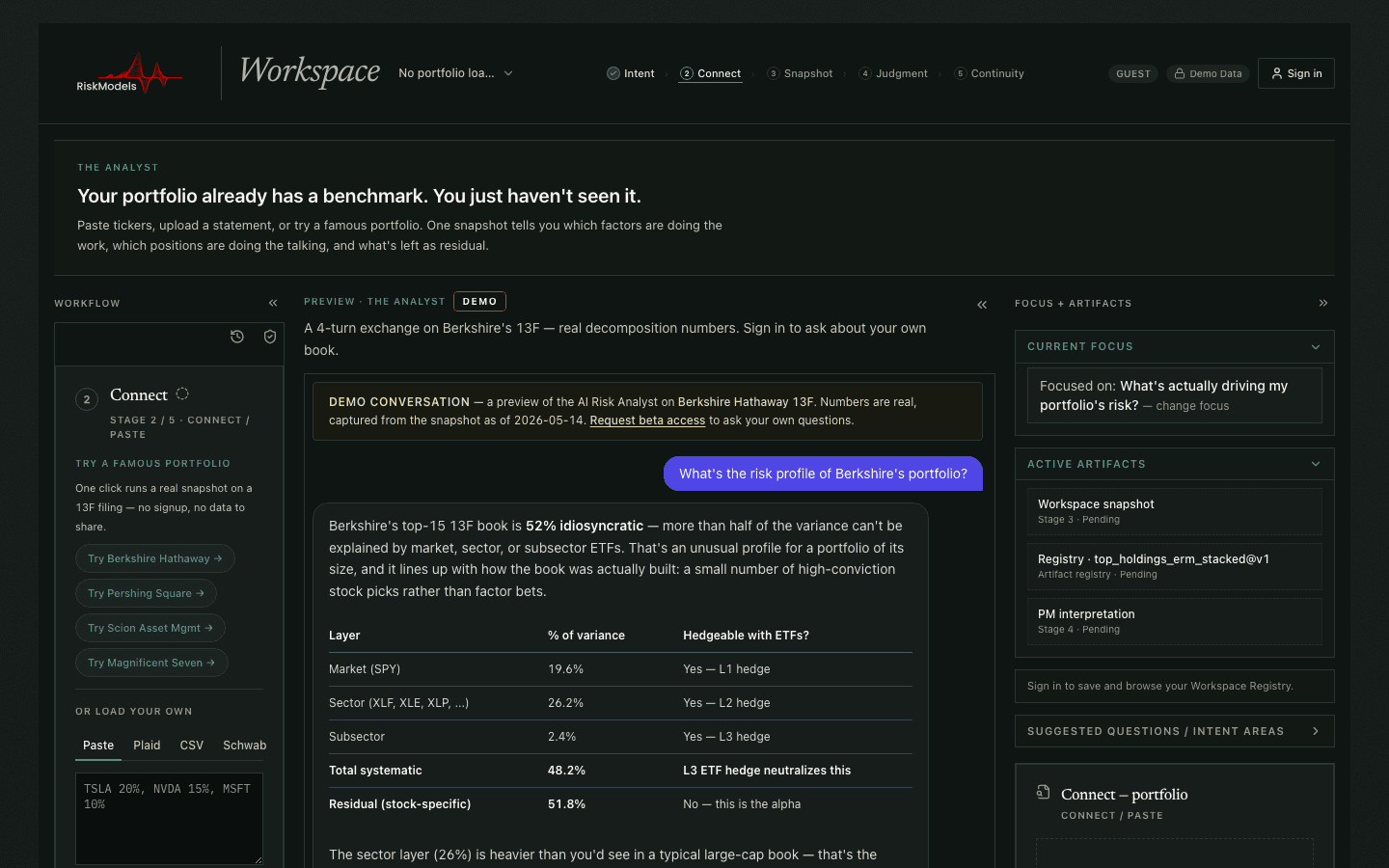

Everything on riskmodels.org is the method. The Analyst Workspace is the product that runs it — currently in active development. You can preview it today at riskmodels.net: open the live demo, explore a loaded book, and see the same market, sector, subsector, and residual decomposition the research is built on. Running it on your own holdings is invite-managed while the product matures.

How to preview it

- 01

Open the preview

Go to riskmodels.net — the demo workspace loads directly. No separate dashboard, no setup, nothing to install.

- 02

Explore the loaded book

A live Berkshire Hathaway book is loaded by default, so you can read the full decomposition output before bringing anything of your own.

- 03

Read the decomposition

The workspace separates every position — and the book as a whole — into market, sector, subsector, and residual variance, then rolls those layers into the benchmark the portfolio actually trades against.

In active development. Anyone can open the workspace and explore the demo. Running it on your own holdings is invite-managed while the product matures — request access from inside the workspace and we will be in touch.

Subscribe to the Quarterly Attribution Review.

Research notes on risk decomposition, fund attribution, 13F filings, and benchmark structure — a few times a quarter.