Workspace

The Analyst Workspace

Everything on riskmodels.org is the method. The Analyst Workspace is where you run it. Bring a portfolio and riskmodels.net returns the same market, sector, subsector, and residual decomposition the research is built on — measured on your own holdings, at a single address, with nothing to install.

How to find it

- 01

Go to riskmodels.net

There is no separate dashboard and no setup step. The home page is the workspace — you land directly in the Analyst Workspace.

- 02

Bring a portfolio

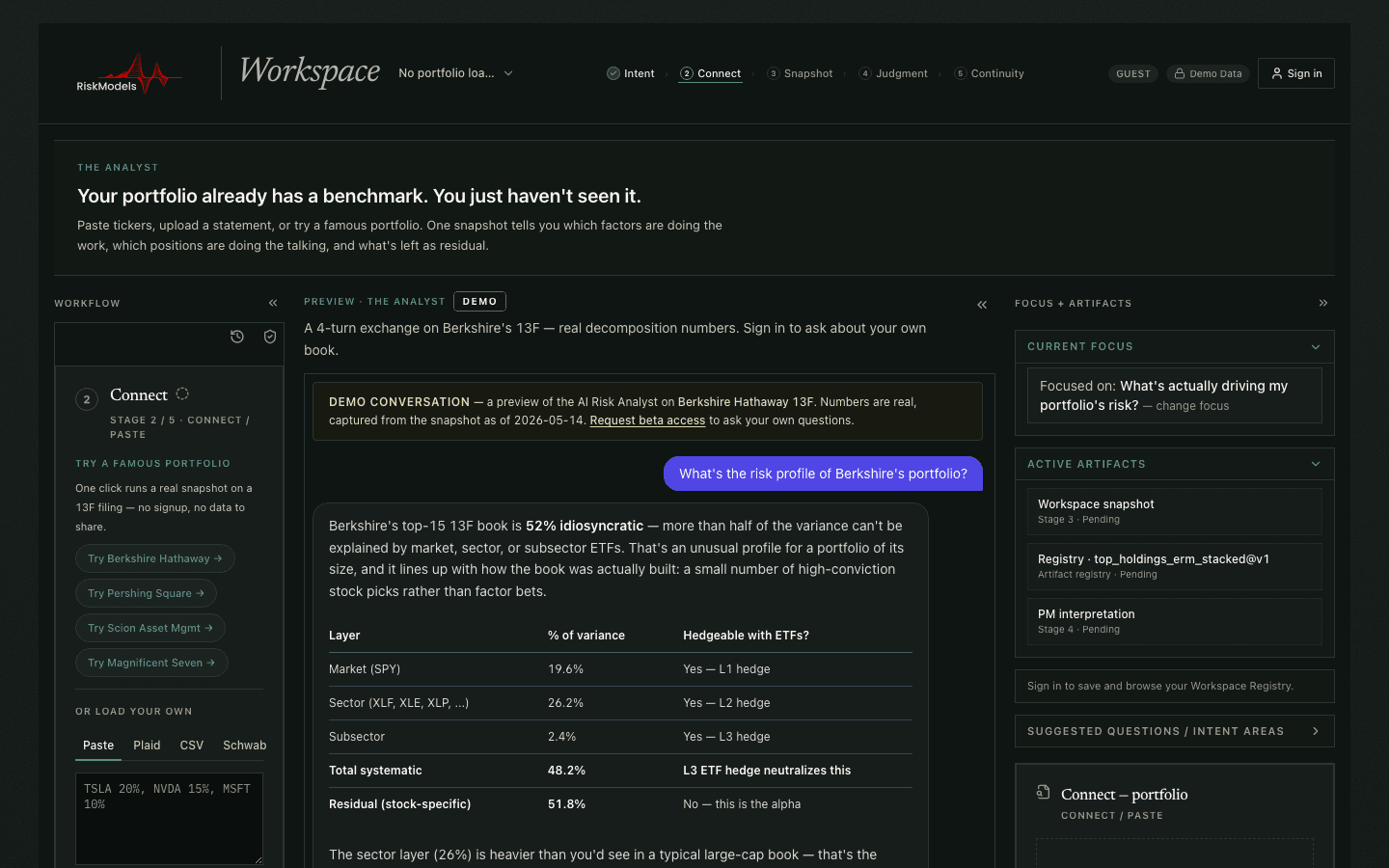

Describe your holdings to the agent in plain language, or import a position list. A live Berkshire Hathaway book is loaded by default, so you can read the full output before committing anything of your own.

- 03

Read the decomposition

The workspace separates every position — and the book as a whole — into market, sector, subsector, and residual variance, then rolls those layers into the benchmark your portfolio actually trades against.

Early beta. Anyone can open the workspace and explore the demo. Running it on your own holdings is invite-managed while the product matures — request access from inside the workspace and we will be in touch.

See the idea move

The decomposition, in two terms

Before you open the workspace, here is the core idea. Total variance splits into a systematic part, β²σ_m², and a residual part, σ_ε². The workspace resolves that residual further into sector and subsector layers; the control below holds it to two so the mechanics stay visible. Units are normalized and illustrative — move the sliders and watch a low headline beta still carry a large residual.

Subscribe to the Quarterly Attribution Review.

Built around the SEC disclosure cycle — see the SEC Filing Calendar for upcoming 13F / 10-K / N-PORT deadlines.